The commercial real estate crisis is looming on the horizon, raising alarms among investors and economists alike. As high office vacancy rates continue to plague major cities, the ramifications extend far beyond a mere decline in property values. The impending wave of commercial real estate loans set to mature by 2025 poses a significant risk to banks that have heavily invested in this sector. With interest rates still elevated, financial experts are concerned that the impact on banks could lead to a cascade of delinquencies, undermining the stability of the broader economy. As the effects of these mounting pressures unfold, a careful examination of the commercial real estate landscape becomes essential for understanding the future economic threats that may arise.

The impending turmoil in the commercial property market is generating widespread concern among stakeholders, signaling a potential crisis for the sector. With rising office vacancies and diminishing demand for physical office spaces, many industry insiders are questioning the sustainability of investments in commercial properties. Financial institutions holding significant portfolios of real estate loans might face severe repercussions if a sudden spike in delinquencies occurs. Furthermore, the ramifications extend to regional banks, which could see their financial stability shaken in light of these economic challenges. As we navigate this complex landscape, it is crucial to consider the interconnected nature of the commercial real estate realm and broader financial systems.

Understanding the Commercial Real Estate Crisis

The commercial real estate crisis is gradually unfolding as we see a sustained increase in office vacancy rates across major U.S. cities. These high vacancy rates, fluctuating between 12% and 23%, show a stark contrast to the pre-pandemic era when demand for office space was much stronger. With the advent of remote and hybrid work models, businesses are opting for reduced spaces or entirely forgoing physical offices. This shift not only drives down property values but also raises concerns about the long-term viability of investments in commercial real estate, creating a precarious environment for stakeholders throughout the market.

Experts are now closely monitoring the potential economic effects stemming from the impending maturity of significant real estate loans, most of which were secured during periods of historically low interest rates. As these loans come due, the consequences for both lenders and the economy could be severe. The likelihood of increased delinquency could threaten the financial stability of institutions heavily invested in the commercial property market, leading to a ripple effect that influences borrowing conditions, consumer lending terms, and ultimately, general economic health.

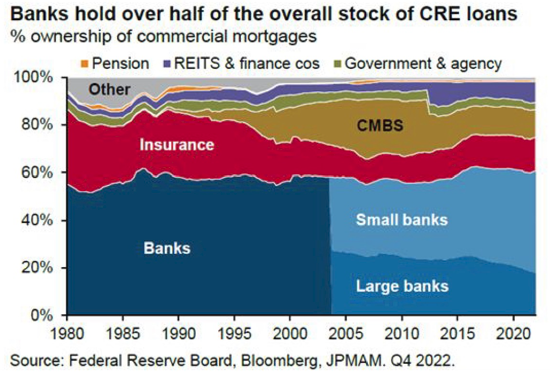

The Impact of Office Vacancy Rates on Banks

High office vacancy rates are raising alarm bells among financial experts, especially regarding their potential impact on banks and financial institutions. As more office buildings sit empty, the value of collateral backing commercial real estate loans diminishes, weakening banks’ balance sheets significantly. This situation is particularly concerning for regional banks that hold substantial portfolios of real estate loans, which could result in increased delinquencies and defaults. With around 20% of commercial mortgage debt due this year, any substantial wave of defaults could strain liquidity and might necessitate a broader reevaluation of lending practices within the banking sector.

Additionally, the rising vacancy rates threaten to trigger a cycle of tighter lending conditions, as banks become more risk-averse, given the economic uncertainty surrounding the commercial real estate market. This tightening of credit could limit access to necessary funds for companies trying to navigate the post-pandemic landscape, further constraining economic growth. As these banks contend with the fallout of a struggling commercial real estate sector, the overall economic climate could experience shifts, potentially affecting employment rates and consumer spending.

Economic Effects of the Commercial Real Estate Decline

The decline in commercial real estate viability poses significant economic effects beyond just the financial sector. Particularly in areas where banks are heavily invested in real estate, local economies could face hardships as lending practices tighten. This could lead to reduced consumption as businesses and consumers navigate decreased availability of credit. With high vacancy rates translating into depressed commercial property values, communities might see potential tax revenue declines, further straining local infrastructures and services essential for public welfare.

However, the overall economic environment remains complex; while multiple sectors ponder the consequences of the commercial real estate crisis, many others are thriving. The current solid job market and booming stock market present a stark contrast to the troubles within commercial properties. Despite the challenges posed by high vacancy rates, some segments of the economy benefit from these shifts, reflecting a dichotomy that makes the broader economic effects difficult to assess.

Interest Rates and Their Role in the Real Estate Crisis

As interest rates remain elevated, the implications for commercial real estate are significant. Higher borrowing costs affect the feasibility of refinancing existing loans, making it harder for property owners to manage their debt burdens. This creates a scenario where many could face defaults on loans, especially as significant real estate debts come due in the next few years. Kenneth Rogoff and other financial experts warn that while the Fed’s hesitation to cut interest rates can stabilize some sectors of the economy, it simultaneously complicates recovery efforts within commercial real estate.

The persistence of high interest rates may also distort market perceptions, where investors might hold onto the hope that rates will decline without adjusting to the current realities of the market. This disconnect creates risks of severe over-leverage as many investors capitalize on previous low rates, thus increasing their potential exposure to losses should economic conditions not improve. The outcome of this precarious balancing act among interest rates, vacancy rates, and loan maturities looms large on the financial landscape as stakeholders brace for possible challenges ahead.

The Role of Banks in Mitigating the Real Estate Crisis

Banks play a critical role in either mitigating or exacerbating the conditions surrounding the commercial real estate crisis. Larger banks, subjected to stringent regulations following the 2008 financial crisis, have substantial resources and diversified portfolios that can weather sector-specific downturns. Their ability to absorb losses without resulting in systemic crises is crucial. However, this is significantly different for smaller banks less capitalized and those without robust risk management practices.

As some regional banks grapple with potential failures due to heavy exposure to commercial real estate, regulatory response and proactive measures will determine the resilience of the banking system. If larger banks can manage their real estate portfolios effectively, they might mitigate widespread economic fallout. However, the fate of smaller institutions, which may face crisis, remains uncertain. More focus on diversified asset management and lending practices could be essential in navigating this turbulent phase for both banks and the economy.

Potential for a Broader Financial Crisis

The commercial real estate situation evokes memories of previous financial crises, as the potential for a broader meltdown continues to fuel concern among investors and analysts alike. While the current climate showcases a substantially different financial landscape, the convergence of high vacancy rates and pending loans due suggests that vulnerabilities exist within the system. If a substantial number of defaults from commercial properties were to occur, the cascading effects could destabilize financial markets, particularly for investors heavily reliant on real estate assets.

Conversely, it is crucial to note that many experts, including Kenneth Rogoff, convey that a complete financial crisis akin to that of 2008 is not necessarily on the horizon. The banking system today is theoretically more resilient and equipped with mechanisms to manage downturns. Still, vigilance is required as the potential for localized downturns in banks could spur broader economic distress if not addressed effectively. The relationship between commercial real estate performance and overall economic stability ensures that continued monitoring of emerging risks is paramount.

Prospects for Recovery in Commercial Real Estate

Despite the prevailing challenges in commercial real estate, there remains a glimmer of hope for recovery. As investors await a reduction in long-term interest rates, some analysts argue that economic revival could stimulate demand for office space, aiding recovery efforts. It’s essential for stakeholders to remain adaptable, focusing on innovative solutions to repurpose and revitalize underutilized properties. Scenarios such as converting vacant office buildings into residential spaces, while logistically complicated, could provide new opportunities and draw tenants back to these locations.

Moreover, maintaining a keen focus on sustainability and modern amenities could attract businesses back to the office, emphasizing a workspace that prioritizes employee wellness and productivity. Those properties equipped with advanced features such as air filtration systems and flexible layouts may withstand economic pressures better than traditional spaces. As the landscape evolves, commercial real estate must adapt to the shifting expectations of tenants and investors, fostering resilience in a post-pandemic world.

Impact of the Commercial Real Estate Crisis on Consumers

The commercial real estate crisis bears implications for the consumer base that extend beyond market dynamics. As banks tighten lending standards due to potential risks in the commercial sector, consumers may face higher borrowing costs or reduced access to loans, limiting their financial flexibility. Additionally, decreased consumer confidence often correlates with broader economic fears; if potential delinquencies in commercial real estate lead to declines in local bank stability, communities could experience diminished access to vital financial services and support.

Furthermore, pension funds heavily invested in commercial real estate could experience significant losses, adversely affecting individuals relying on pensions for retirement. Such scenarios highlight an interconnected financial ecosystem where sector-specific troubles can cascade through various consumer sectors. Policymakers and financial regulators need to assess the broader implications of a struggling commercial real estate market, ultimately safeguarding consumers against downstream risks.

Navigating the Future of Commercial Real Estate Investments

Looking ahead, navigating the future of commercial real estate investments requires a discerning approach. Investors and stakeholders must incorporate better risk assessment practices when evaluating properties, particularly given the fluctuations in vacancy rates and changing economic conditions. A robust analysis that can account for economic indicators, interest rate trends, and local demand is essential for minimizing potential losses and enhancing performance.

In addition, embracing technology and innovative investment models can present new opportunities in this sector. Adaptive reuse of existing spaces to meet evolving market demands aligns with sustainability trends and consumer preferences, potentially positioning investors favorably for future growth. By focusing on these strategies, stakeholders can better position themselves to circumvent potential crises and enhance the overall resilience of the commercial real estate market.

Frequently Asked Questions

How do high office vacancy rates contribute to the commercial real estate crisis?

High office vacancy rates directly impact the commercial real estate crisis by devaluing properties, reducing rental income, and escalating financial strain on investors. As occupancy rates remain below pre-pandemic levels, particularly in major cities, property values drop, leading to potential defaults on commercial loans.

What impact do rising interest rates have on the commercial real estate crisis?

Rising interest rates exacerbate the commercial real estate crisis by increasing borrowing costs for real estate loans. Investors face higher expenses for refinancing existing debt, which causes more financial strain, especially among over-leveraged properties struggling with low occupancy.

What are the potential economic effects of a commercial real estate crisis?

The economic effects of a commercial real estate crisis include losses for investors, particularly in pension funds, reduced lending from affected banks, and a possible slowdown in consumer spending. These issues can create a ripple effect, leading to job losses and decreased economic growth.

How could the impact on banks worsen due to the commercial real estate crisis?

The commercial real estate crisis could worsen the impact on banks as a wave of delinquent loans emerges, particularly in regional banks less exposed to strict regulations. This could lead to significant losses, tighter lending conditions, and possible bank failures, particularly if a recession occurs.

What financial risks do banks face from the commercial real estate crisis and high vacancy rates?

Banks face financial risks from the commercial real estate crisis primarily through exposure to a high volume of delinquent property loans tied to high vacancy rates. As property values decline, banks may need to absorb significant losses, adversely affecting their balance sheets and overall financial stability.

Can the commercial real estate crisis lead to a repeat of the 2008 financial crisis?

While the commercial real estate crisis poses risks, experts believe it is unlikely to lead to a repeat of the 2008 financial crisis. The regulatory environment for banks has improved since then, although specific regional banks may still face severe challenges caused by defaulting real estate loans.

What measures could be taken to mitigate the commercial real estate crisis?

To mitigate the commercial real estate crisis, lowering long-term interest rates would be beneficial for allowing refinancing of loans. Additionally, innovative strategies such as repurposing vacant office buildings into residential spaces could help revitalize the sector and reduce vacancy rates.

What is the connection between commercial real estate loans and the overall banking sector?

Commercial real estate loans constitute a significant portion of banks’ assets, typically around 25%. A considerable impact on these loans, due to the commercial real estate crisis, can lead to heightened risks for banks, particularly those heavily invested in this sector, potentially affecting their solvency.

| Key Point | Details |

|---|---|

| High Office Vacancy Rates | Vacancy rates in major U.S. cities range from 12% to 23%, affecting property values. |

| Commercial Real Estate Loans Due | 20% of the $4.7 trillion in commercial mortgage debt is due this year, posing risks to banks and the economy. |

| Potential Bank Failures | While losses are expected, a full-blown financial crisis similar to 2008 is not likely due to regulatory measures on larger banks. |

| Impact on Local Banks | Smaller banks, less regulated, may face significant challenges leading to potential failures affecting local economies. |

| Optimism Among Investors | Some investors believe interest rates will decline, allowing recovery by 2025, despite current risks. |

| Regional Bank Vulnerabilities | Regional banks heavily invested in commercial real estate could face significant losses from delinquent loans. |

| Broader Economic Climate | Despite struggles in commercial real estate, the overall economy appears solid due to a strong job market and stock performance. |

Summary

The commercial real estate crisis poses significant challenges for the economy, particularly with high office vacancy rates and a substantial amount of commercial loans coming due. However, while this situation may negatively impact regional banks and cause local economic hardships, the larger banking sector, especially the major banks, seems well positioned to absorb these shocks. As we analyze the unfolding events, it is essential to monitor the situation closely, as any significant economic downturn could exacerbate the existing issues within commercial real estate.