Corporate tax reform is emerging as a pivotal topic in the ongoing political discourse surrounding the economic strategies of the United States. As key provisions of the 2017 Tax Cuts and Jobs Act, which significantly lowered corporate tax rates, approach their expiration, lawmakers are faced with a crucial decision: should they renew these cuts or reconsider the corporate tax framework altogether? The potential economic impact of tax cuts is being debated vigorously, as economists analyze findings from research by Gabriel Chodorow-Reich and others. Their work illustrates the balance between stimulating corporate investment and the crucial need for sustaining tax revenue. With the stakes high and partisan divides looming, the discussion around corporate tax reform is expected to intensify as 2025 approaches.

The conversation around business taxation reform, often referred to as corporate tax restructuring, is currently gaining traction in the political landscape. With the expiration of various provisions from the 2017 Tax Cuts and Jobs Act drawing nearer, Congress faces pressing questions about the future of corporate tax regulation. The discourse focuses not only on the adjustments to corporate tax rates but also on their wider economic implications for investment and revenue generation. Leading economic figures, including Gabriel Chodorow-Reich, are critically examining the outcomes of past tax cuts to inform potential future policies. As lawmakers grapple with these issues, the impacts on economic growth and corporate tax revenue remain at the forefront of the national conversation.

The Economic Impact of the Tax Cuts and Jobs Act

The Tax Cuts and Jobs Act (TCJA), enacted in 2017, represented a fundamental shift in U.S. tax policy, predominantly reducing corporate tax rates from 35% to 21%. This significant reduction was touted by proponents as a means to stimulate economic growth, increase wages, and boost corporate investment. However, a close examination of its economic impact reveals a more nuanced reality. According to economist Gabriel Chodorow-Reich, while corporate investments saw an increase of approximately 11%, many of these gains were attributable to targeted measures like business expensing rather than broad tax cuts. The notion that corporate tax cuts would entirely pay for themselves through enhanced business activity has not been supported by the data; thus, the actual economic benefits were less pronounced than initially anticipated.

With the looming expiration of several key TCJA provisions, including those related to corporate tax rates and household tax credits, the debate surrounding the economic impact of this tax reform is set to intensify in the upcoming election year. As a bipartisan discussion unfolds in Congress, voters are likely to prioritize the renewal of provisions that directly affect their financial situations. However, the overall consequences on corporate behavior and federal revenue generation must be scrutinized carefully. The TCJA initially led to a dramatic decrease in corporate tax revenue—a staggering 40% drop—which raises questions about its long-term sustainability and effectiveness in fostering genuine economic growth.

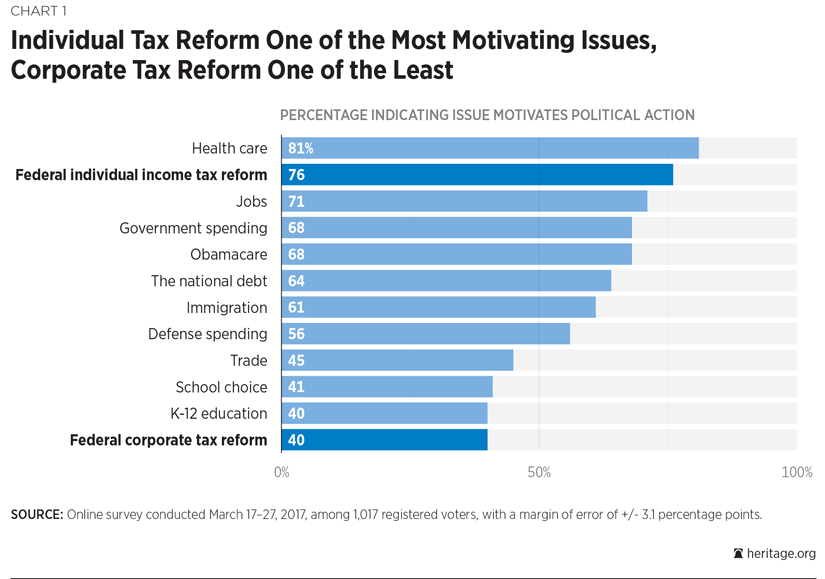

Corporate Tax Reform: A Necessary Discussion

As we approach potential discussions on corporate tax reform within the broader tax landscape, the insights from Gabriel Chodorow-Reich’s recent analysis are invaluable. By highlighting the complexities surrounding the impact of the TCJA, Chodorow-Reich emphasizes the necessity of evaluating both the intended and unintended consequences of such legislative actions. His findings indicate that while business investments did grow, this growth was significantly influenced by particular provisions rather than the overarching tax rate cuts. This distinction is critical for lawmakers as they deliberate whether to raise corporate tax rates in order to finance social initiatives or further cut them to drive investment.

Moreover, the discourse surrounding corporate tax reform calls into question not only the effects of lower rates on corporate behavior but also the implications for federal tax revenues and public services. With a projected revenue decrease of $100 billion to $150 billion annually due to the TCJA, the argument for raising corporate tax rates becomes compelling, especially if lawmakers aim to mitigate budget shortfalls following the expiration of significant tax provisions. Ultimately, the future of corporate tax reform hinges on a balanced approach that considers economic data, revenue needs, and the societal responsibilities of corporations.

Understanding Corporate Tax Revenue Dynamics

The fluctuations in corporate tax revenue following the enactment of the TCJA present a complex narrative of economic adaptation amid changing tax policies. Initially, corporate tax revenue plummeted by 40% once the reforms were implemented, leading to fears of long-term fiscal instability. However, recent trends observed by Chodorow-Reich suggest a rebound in corporate profits, with revenues climbing higher than anticipated in the wake of the pandemic. This resurgence raises critical questions about the functionality of lowered tax rates in a modern economic context.

As corporate tax revenue began to recover, driven in part by businesses adjusting their strategies, including shifting profits back to the U.S., there remains uncertainty surrounding the mechanisms facilitating this rebound. Factors such as global economic pressures, competitive international tax strategies, and internal adjustments within corporations are likely contributors. Chodorow-Reich’s call for further research into these developments suggests that understanding the dynamics of corporate taxation will be key to crafting future improvements, particularly as the government grapples with the balancing act of fostering growth while ensuring adequate funding for essential services.

Investments, Wages, and Corporate Tax Policy

The relationship between corporate tax policy, investments, and wages is a focal point in the analysis of the TCJA. With cuts to corporate tax rates, a primary goal was to stimulate increased business investments that would, in turn, raise wages for employees. Chodorow-Reich’s assessment indicates that while there was a measurable uptick in investment due to provisions like expensing, the anticipated wage growth fell short of early predictions. The research cites a modest average annual increase of $750 per employee, contrasting sharply with previous estimates of $4,000 to $9,000.

The findings imply that while corporate tax cuts can incentivize capital investment, the direct benefits to wages may be less substantial than proponents claimed. By examining how corporate tax structure affects the labor market, policymakers can better understand the multifaceted impacts of tax reform. Moving forward, creating a corporate tax strategy that encompasses both robust investment incentives and realistic expectations for wage growth will be essential in creating a balanced and prosperous economy for all stakeholders.

Navigating Political Landscape and the Future of Corporate Tax Rates

The political landscape surrounding corporate tax rates is becoming increasingly polarized as upcoming elections approach. On one side, advocates of maintaining or further lowering corporate taxes argue that such measures will stimulate growth and competitiveness. On the other, opponents stress the need for higher rates to fund essential public services and initiatives that could benefit society at large. As highlighted in discussions from leaders such as Kamala Harris and Donald Trump, corporate tax reform debates will likely feature prominently in campaign narratives.

As both parties leverage the corporate tax issue for electoral gain, it is crucial for voters to be informed about the economic realities businesses face under different tax regimes. Chodorow-Reich’s work serves as a reminder that real data and thorough economic analysis must guide these conversations. Crafting a policy that responds to the needs of businesses while ensuring that tax revenue adequately supports public interests will be vital as lawmakers chart a path forward in the complex realm of corporate tax reform.

Corporate Innovation: Tax Codes and Investment Incentives

Corporate innovation is a vital aspect of economic growth, and the structure of tax codes can significantly influence the level of investment in research and development. Analyzing the TCJA, Chodorow-Reich and his co-authors found that provisions allowing immediate write-offs of new capital expenditures fostered business innovation more effectively than mere rate cuts. This insight reveals the importance of not only the rate at which corporations are taxed but also the incentives embedded within the tax framework.

If lawmakers aim to enhance corporate investment and drive innovation, a strategic approach to tax reform should prioritize measures that directly encourage business growth. As illustrated by the performance of various tax provisions, a balanced focus on targeted allowances for research and development, alongside thoughtful corporate tax rates, may offer a more effective route toward fostering a culture of continuous innovation within the competitive U.S. market.

Analyzing the Expiring Provisions of the TCJA

The upcoming expiration of the TCJA’s provisions poses challenges and opportunities for lawmakers and businesses alike. Many of the tax cuts aimed at businesses are set to phase out in the coming years, compelling leaders to evaluate their economic impact and the role they play in the broader tax landscape. This review is particularly critical as businesses navigate the aftermath of the pandemic, adjusting to newfound economic realities and fluctuating market demands.

In assessing which provisions should be renewed or adjusted, a comprehensive analysis of their effectiveness in promoting corporate investment and sustaining tax revenues is essential. Engaging with data-driven insights, such as those presented by Chodorow-Reich, can aid in fostering informed decisions that address both the immediate fiscal needs and long-term economic growth objectives. Tailoring corporate tax policies to reflect evolving economic conditions will ensure a responsive and responsible approach to taxation.

The Role of International Competition in Corporate Taxation

As highlighted by Chodorow-Reich, the globalize nature of the modern economy necessitates an understanding of how international competition influences U.S. corporate taxation. The 2017 TCJA aimed to better position U.S. corporations against foreign counterparts, particularly as global tax rates shifted. In this landscape, maintaining competitive corporate tax rates is fundamental to attracting and retaining business investments within the U.S. economy.

Additionally, with countries like Ireland adjusting their low corporate tax rates to compete in the global market, U.S. policymakers must be vigilant. The choices made regarding corporate tax structure will not only influence domestic investment but also the global positioning of U.S. firms. Crafting a tax regime that is both competitive internationally and equitable domestically will be critical in sustaining growth and addressing revenue needs.

Concluding Remarks on Corporate Tax Reform Dialogues

In conclusion, the dialogues surrounding corporate tax reform are complex and multifaceted, reflecting both economic realities and political aspirations. As the TCJA approaches its 2025 deadline for key provisions, the analysis provided by Gabriel Chodorow-Reich serves as a critical touchstone for understanding the intricacies of corporate taxation. With significant implications for investment, wages, and overall economic health, the outcomes of these discussions will play a decisive role in shaping the nation’s fiscal future.

Ultimately, beyond political rhetoric, the need for informed, evidence-based policy decisions is paramount. As lawmakers grapple with the decision to raise or lower corporate tax rates, they must consider the broader implications of their choices on economic growth, corporate responsibility, and public welfare. Engaging with thorough analysis and diverse perspectives will enable a more nuanced approach, ensuring that tax reform aligns with the overarching goal of fostering a robust and equitable economy.

Frequently Asked Questions

What are the main impacts of the 2017 Tax Cuts and Jobs Act on corporate tax rates?

The 2017 Tax Cuts and Jobs Act significantly reduced corporate tax rates from 35% to 21%. This change aimed to stimulate economic growth and investment by making the U.S. tax environment more competitive globally. However, studies, including those by economists Gabriel Chodorow-Reich, indicate that while there was a temporary increase in corporate investments, the long-term impact on wage growth and overall tax revenue was modest.

How has corporate tax revenue changed since the Tax Cuts and Jobs Act was implemented?

After the implementation of the Tax Cuts and Jobs Act, corporate tax revenue initially dropped by about 40%. However, by 2020, corporate tax revenue began to recover, surpassing earlier predictions as business profits increased, partly due to adaptations in the market during the pandemic.

What are some criticisms of the corporate tax cuts introduced by the Tax Cuts and Jobs Act?

Critics of the corporate tax cuts included economists like Gabriel Chodorow-Reich, who argue that the expected significant increases in wages and investment did not materialize to the extent proponents suggested. The findings indicate that while firms responded to tax policy changes, the benefits did not fully offset the dramatic loss in corporate tax revenue.

Did the Tax Cuts and Jobs Act lead to a significant increase in wages for employees as promised?

Predictions prior to the Tax Cuts and Jobs Act suggested wage increases could reach $4,000 to $9,000 per employee. However, comprehensive analyses have shown that the actual increase was closer to $750 per employee in 2017 dollars, highlighting a discrepancy between expectations and actual outcomes.

What role does Gabriel Chodorow-Reich play in the discussion about corporate tax reform?

Gabriel Chodorow-Reich, a Harvard macroeconomist, has conducted extensive research on the impacts of the Tax Cuts and Jobs Act. His work aims to provide a clear analysis of the economic effects of corporate tax cuts, emphasizing the importance of effective tax policy in driving investment without excessively harming government revenue.

How does the expiration of certain provisions in the Tax Cuts and Jobs Act impact corporate tax reform debates?

As key provisions of the Tax Cuts and Jobs Act are set to expire including certain corporate tax benefits, debates around corporate tax reform are intensifying. Lawmakers are discussing potential adjustments to corporate tax rates to balance revenue needs with the desire to foster business growth and investment.

What economic evidence exists regarding the effectiveness of corporate tax cuts on investment?

Research including findings from Gabriel Chodorow-Reich suggests that while capital investments increased by approximately 11% following the Tax Cuts and Jobs Act, the most effective provisions were those allowing immediate expensing of investments, rather than broad statutory tax rate reductions.

| Key Point | Details |

|---|---|

| Corporate Tax Rate Changes | The TCJA permanently reduced the corporate tax rate from 35% to 21%. |

| Impact on Revenue | Predicted reduction in federal corporate tax revenue by $100 billion to $150 billion per year over the next 10 years. |

| Business Investments | Capital investments increased by about 11% due to TCJA, especially from provisions allowing immediate expensing of capital investments. |

| Wage Impact | Wages increased modestly, with estimates showing a potential increase of $750 per year in 2017 dollars, compared to initial predictions of $4,000 to $9,000. |

| Partisan Debate | The TCJA has become a focal point for political debate, with calls from Democrats for raising corporate taxes and Republicans advocating for further cuts. |

Summary

Corporate tax reform remains a critical topic as the U.S. faces expiring provisions from the 2017 Tax Cuts and Jobs Act. The debate highlights differing views on whether raising rates or further cuts will stimulate the economy. Analysis shows that while some business investments did increase post-TCJA, the overall impact on wages and revenue remains contested. Key insights reveal that restoring effective tax provisions may be more beneficial than merely adjusting rates. As the 2025 tax battle approaches, the challenge will be finding a balanced approach that addresses corporate revenue needs while fostering economic growth.